Financial Time Series Models (ARCH/GARCH)

Unlike preceding tabs, in this page I will mainly focus on using Autoregressive Conditional Heteroskedasticity model (ARCH), a useful financial time series model, to study the stock price of Walmart since 2010, rather than forecasting the weekly sales as usual. Financial time series data refers to the data collected over time and indicates the changes of financial variables, including stock prices, interest rates, and other financial indicators. A special characteristic of financial time series is that there often exists volatility in the data, and the volatility tends to cluster over time. Under this circumstance, ARCH and GARCH models can be ideal to study the financial time series, since they can take the volatility into consideration.

In this project, I will first train an ARIMA model, and then utilize ARCH or GARCH to fit the residuals of ARIMA model. Thus, the final model for studying this stock price data can be an ARIMA+ARCH/ARIMA+GARCH model.

1 Data gathering and visualization

First, get the stock price data of Walmart from yahoo.

Code

getSymbols("WMT", from="2010-01-01", to="2023-05-02", src="yahoo")[1] "WMT"Code

head(WMT) WMT.Open WMT.High WMT.Low WMT.Close WMT.Volume WMT.Adjusted

2010-01-04 53.74 54.67 53.67 54.23 20753100 40.01306

2010-01-05 54.09 54.19 53.57 53.69 15648400 39.61462

2010-01-06 53.50 53.83 53.42 53.57 12517200 39.52609

2010-01-07 53.72 53.75 53.26 53.60 10662700 39.54823

2010-01-08 53.43 53.53 53.02 53.33 11363200 39.34901

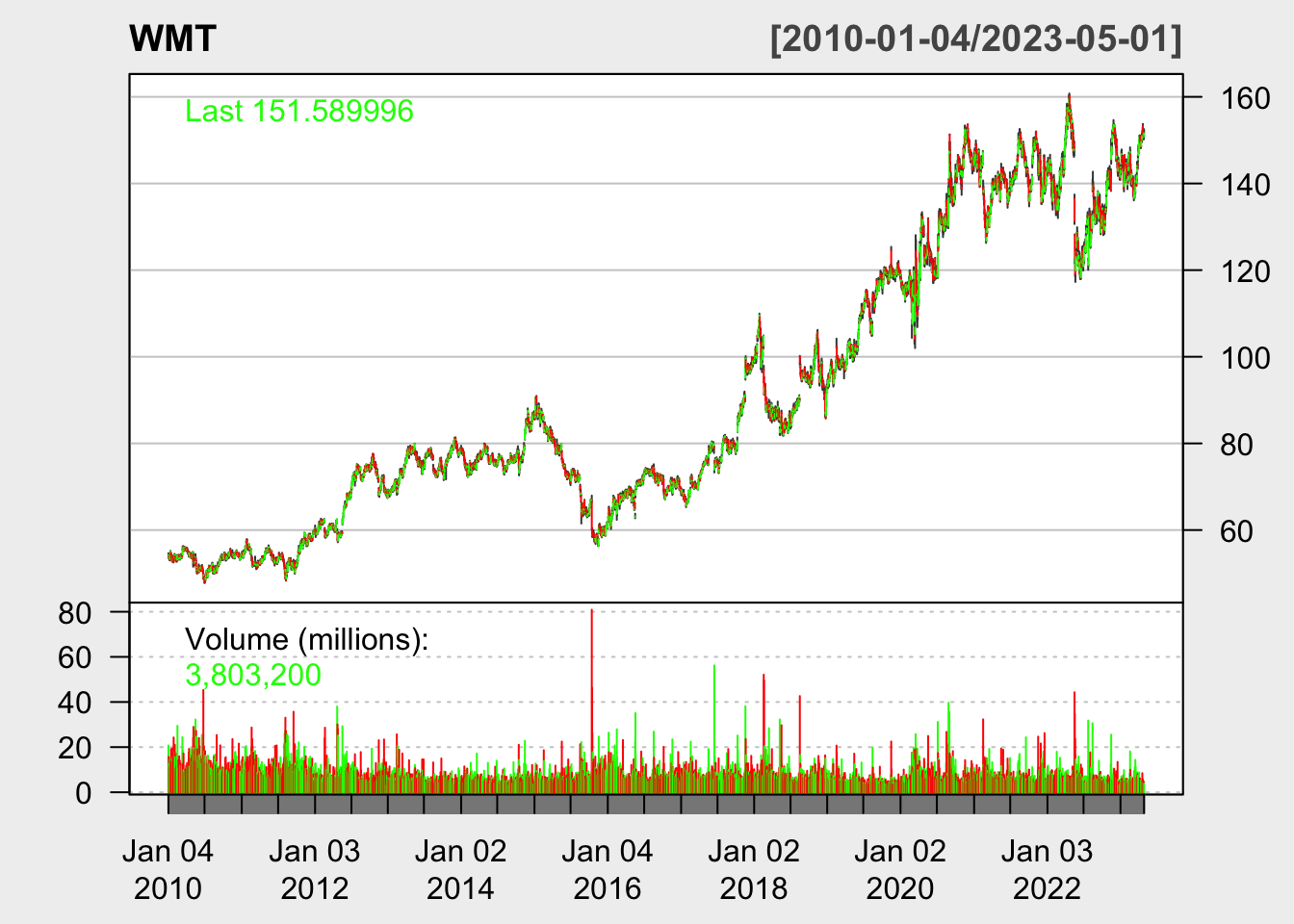

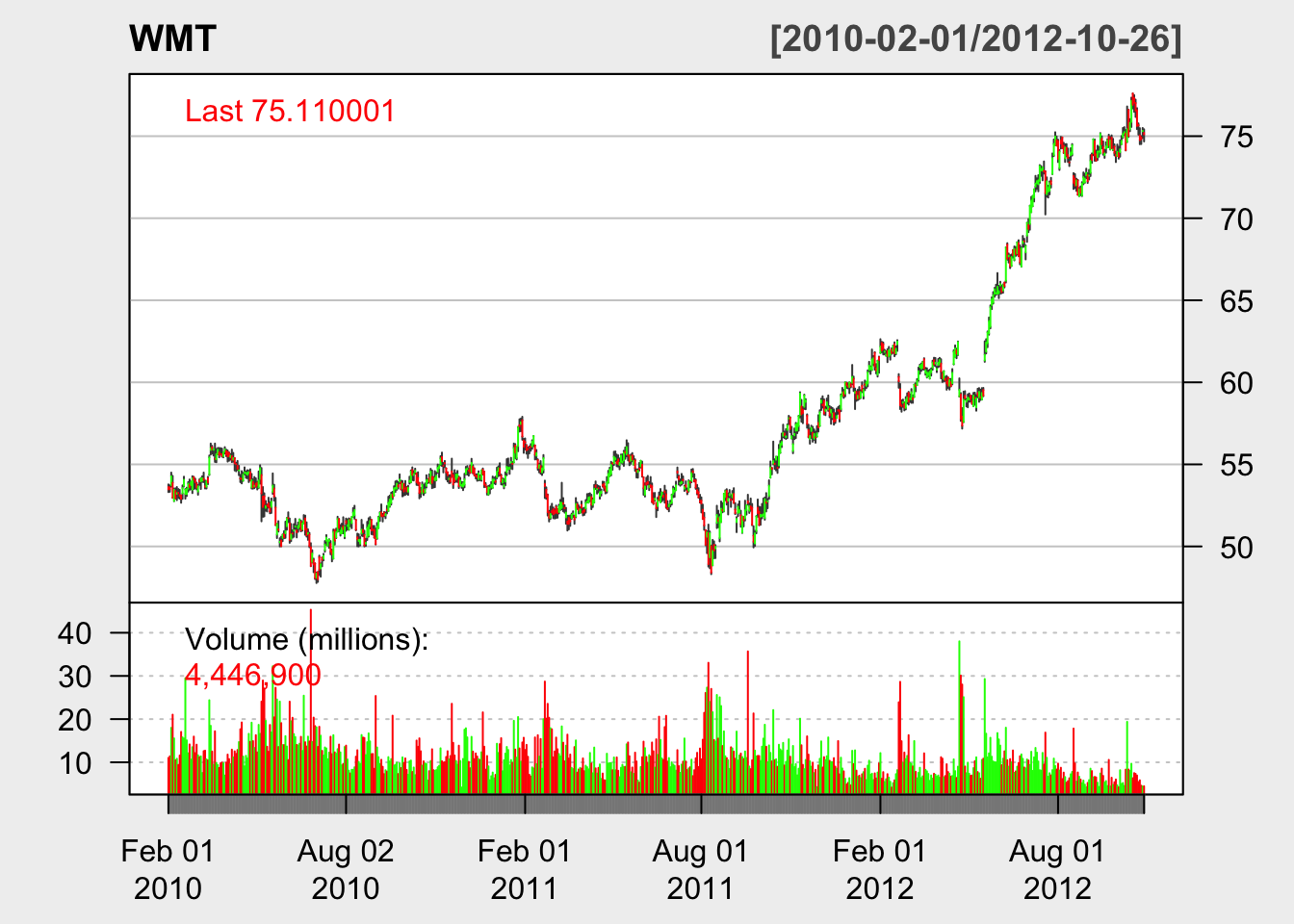

2010-01-11 53.33 54.44 53.10 54.21 13987700 39.99831Here is candlestick plot showing the stock price of Walmart since 2010:

Code

chartSeries(WMT, theme = chartTheme("white"),

bar.type = "hlc",

up.col = "green",

dn.col = "red")

According to this plot, we first notice the upward trend of this stock price within the past decade. Also, this plot shows increasing volatility in the data over time.

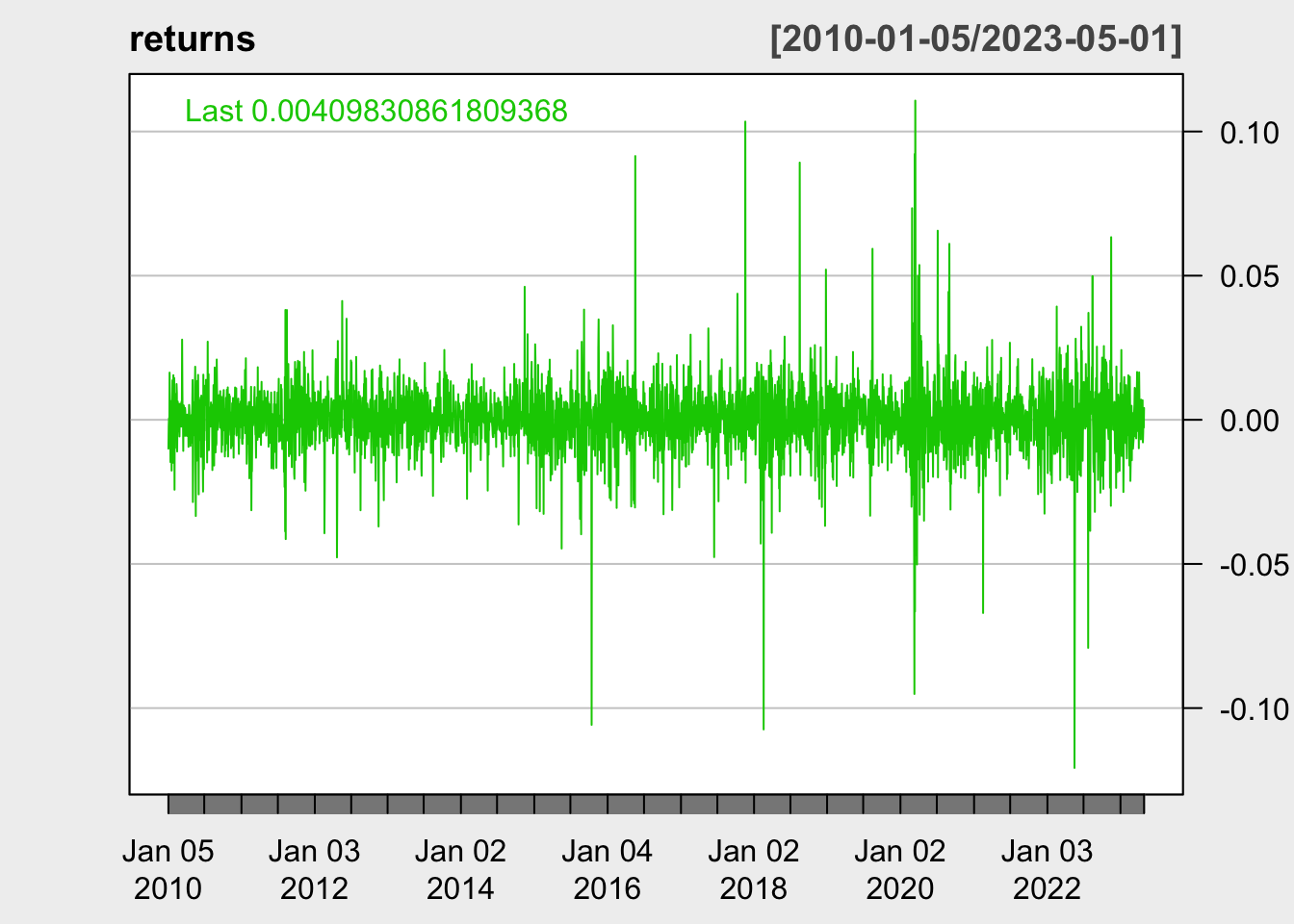

Following plot will apply the log function and a first order differencing to the data, which makes it much easier to notice the change in volatility.

Code

WMT.close<- Ad(WMT)

returns = diff(log(WMT.close))

chartSeries(returns, theme="white")

We can clearly see that volatility has greatly increased by years, especially at around 2020. Therefore, an ARCH or GARCH model will be appropriate for studying this data. Now let’s first look at the ACF/PACF plot to check if an ARIMA model is necessary before fitting an ARCH.

2 ACF/PACF plots

Code

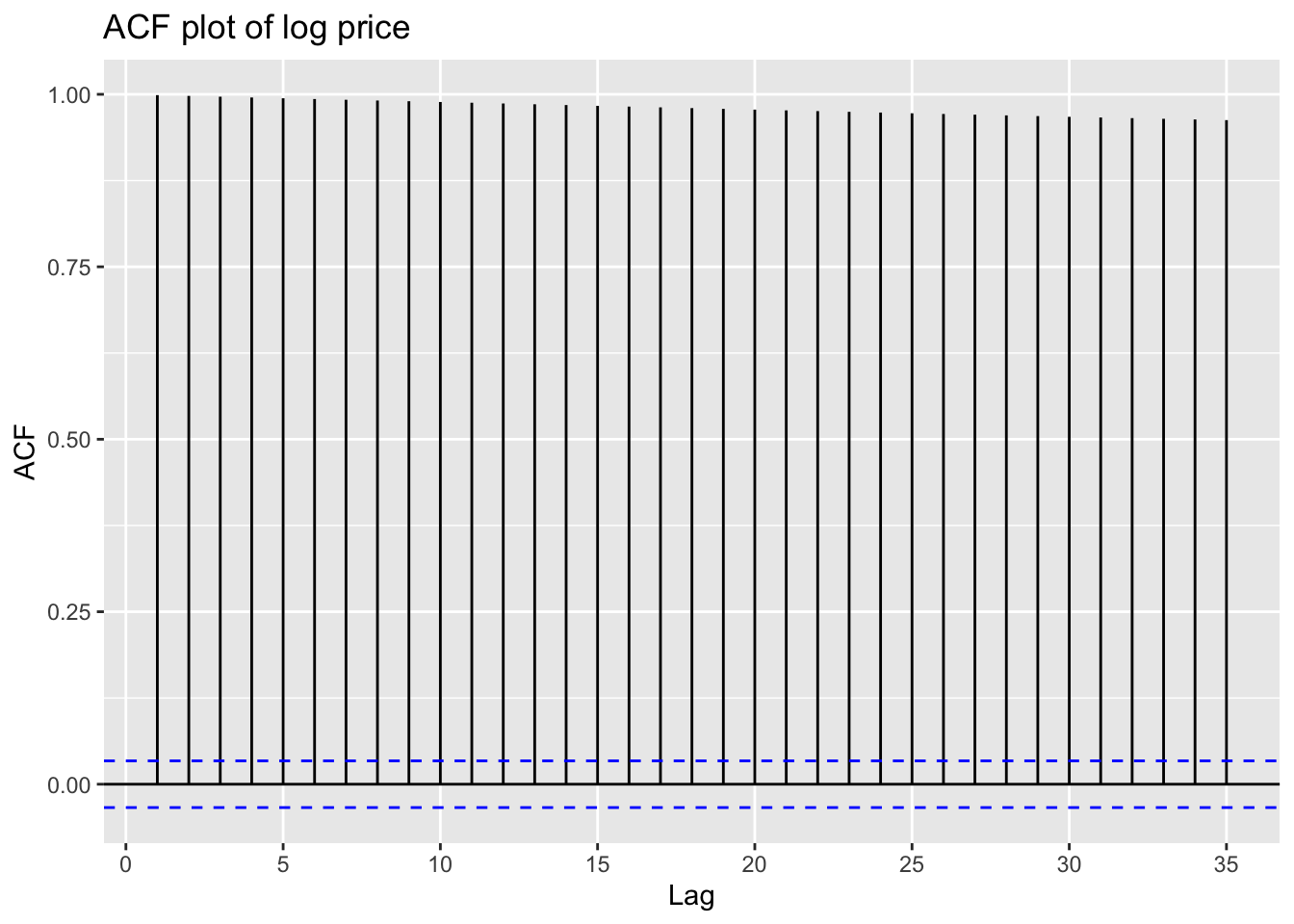

ggAcf(log(WMT.close))+ggtitle("ACF plot of log price")

From this plot, it is evident that a differencing must be applied to this stock price data.

Code

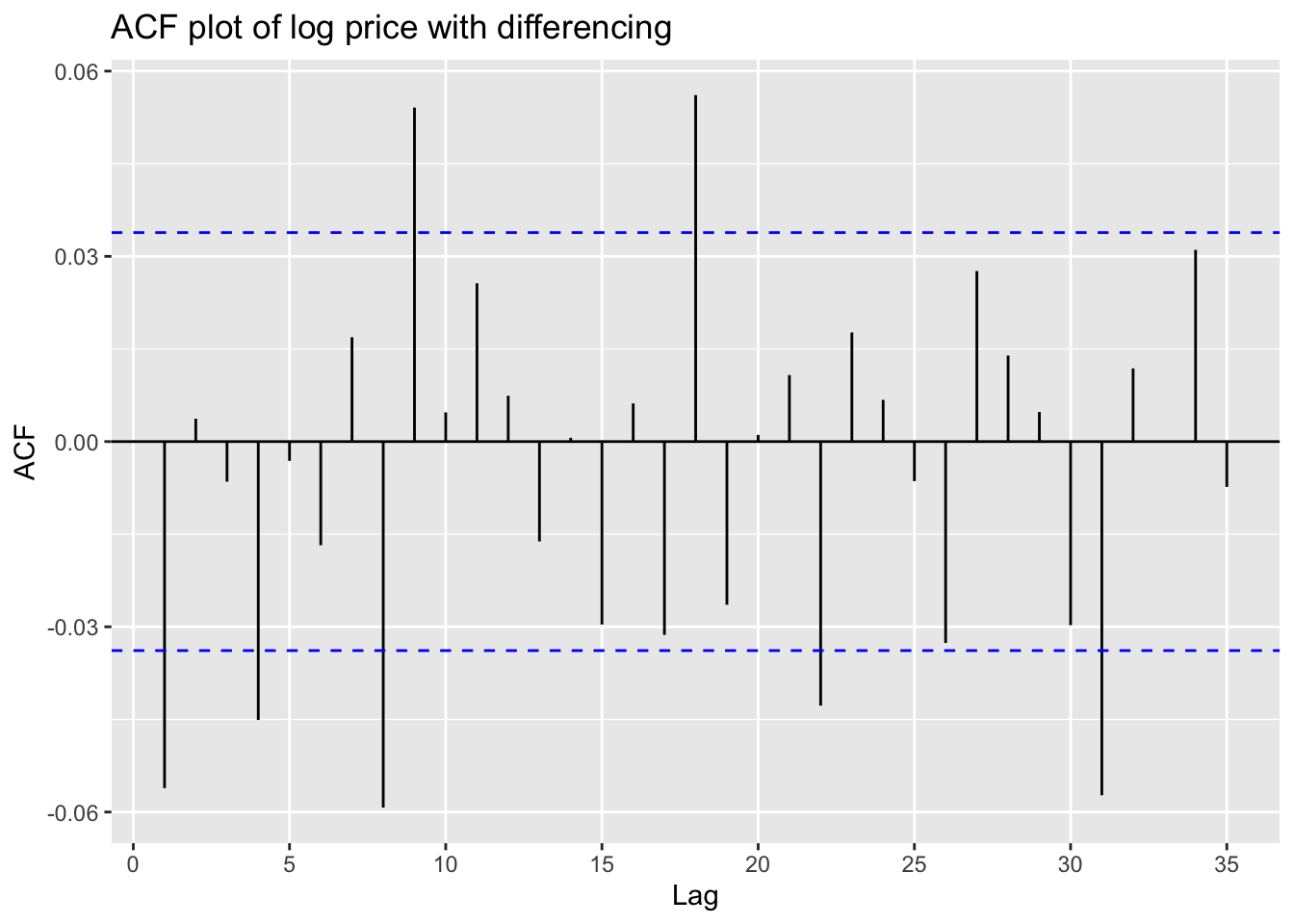

ggAcf(returns)+ggtitle("ACF plot of log price with differencing")

Code

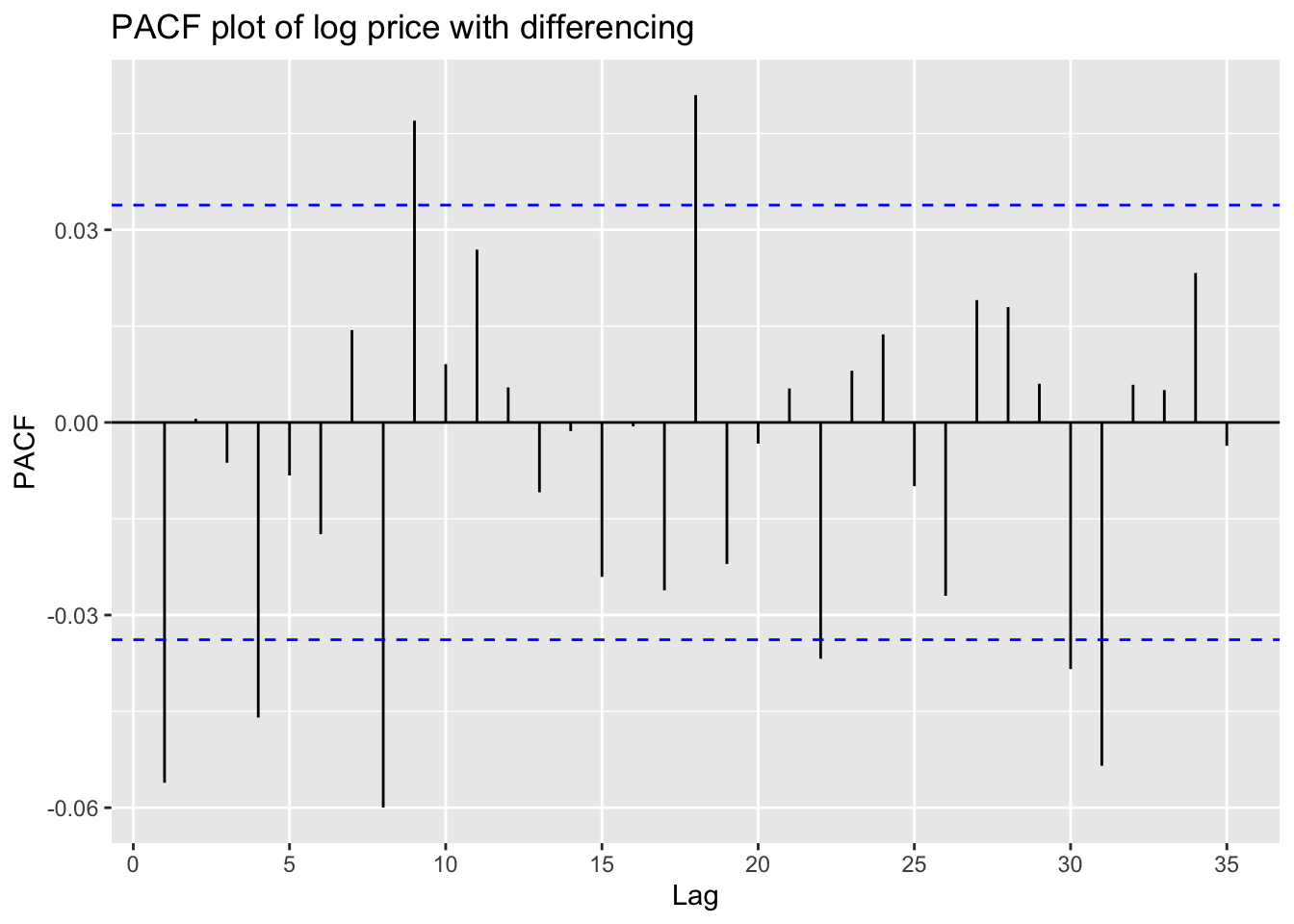

ggPacf(returns)+ggtitle("PACF plot of log price with differencing")

Code

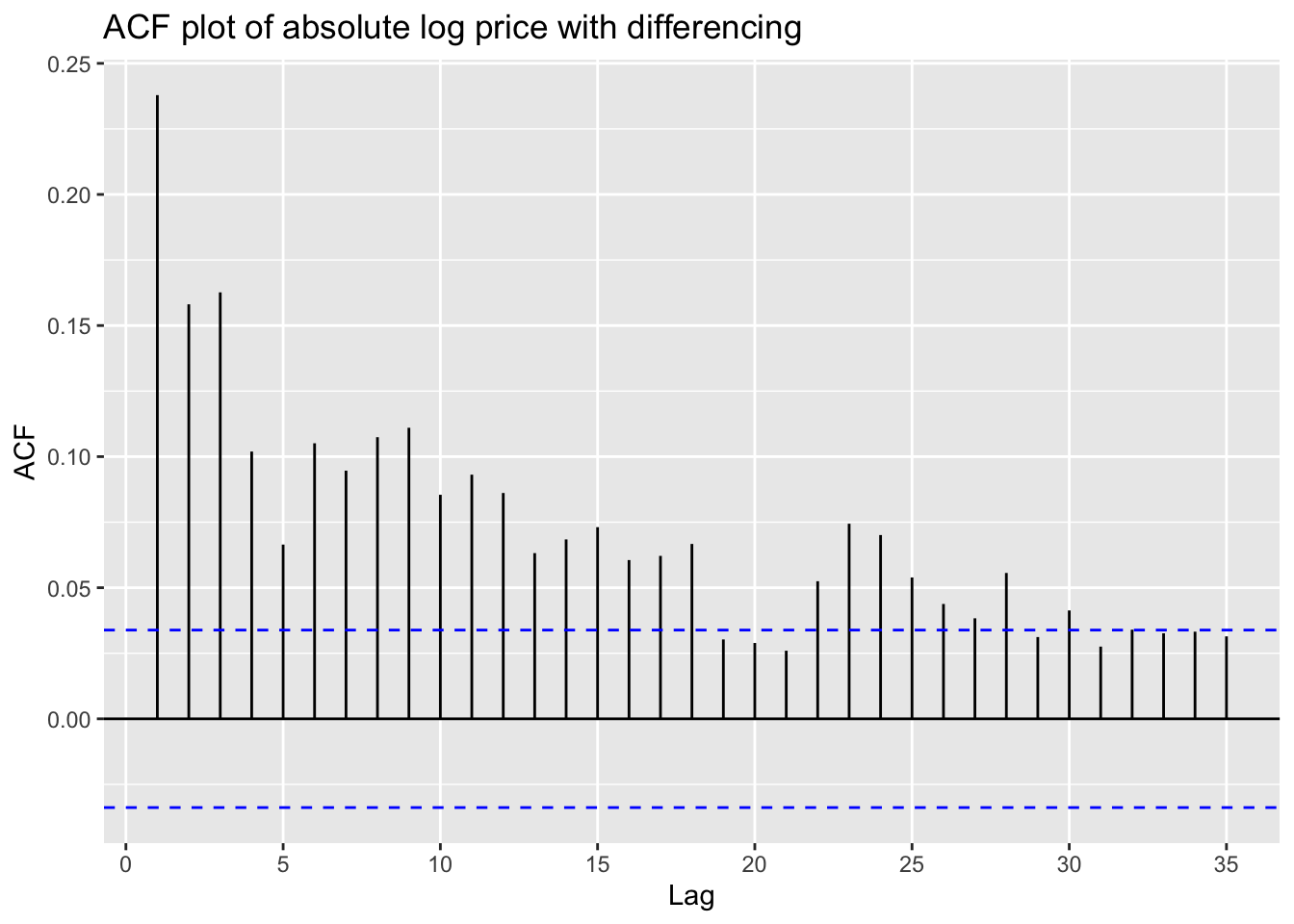

ggAcf(abs(returns))+ggtitle("ACF plot of absolute log price with differencing")

Code

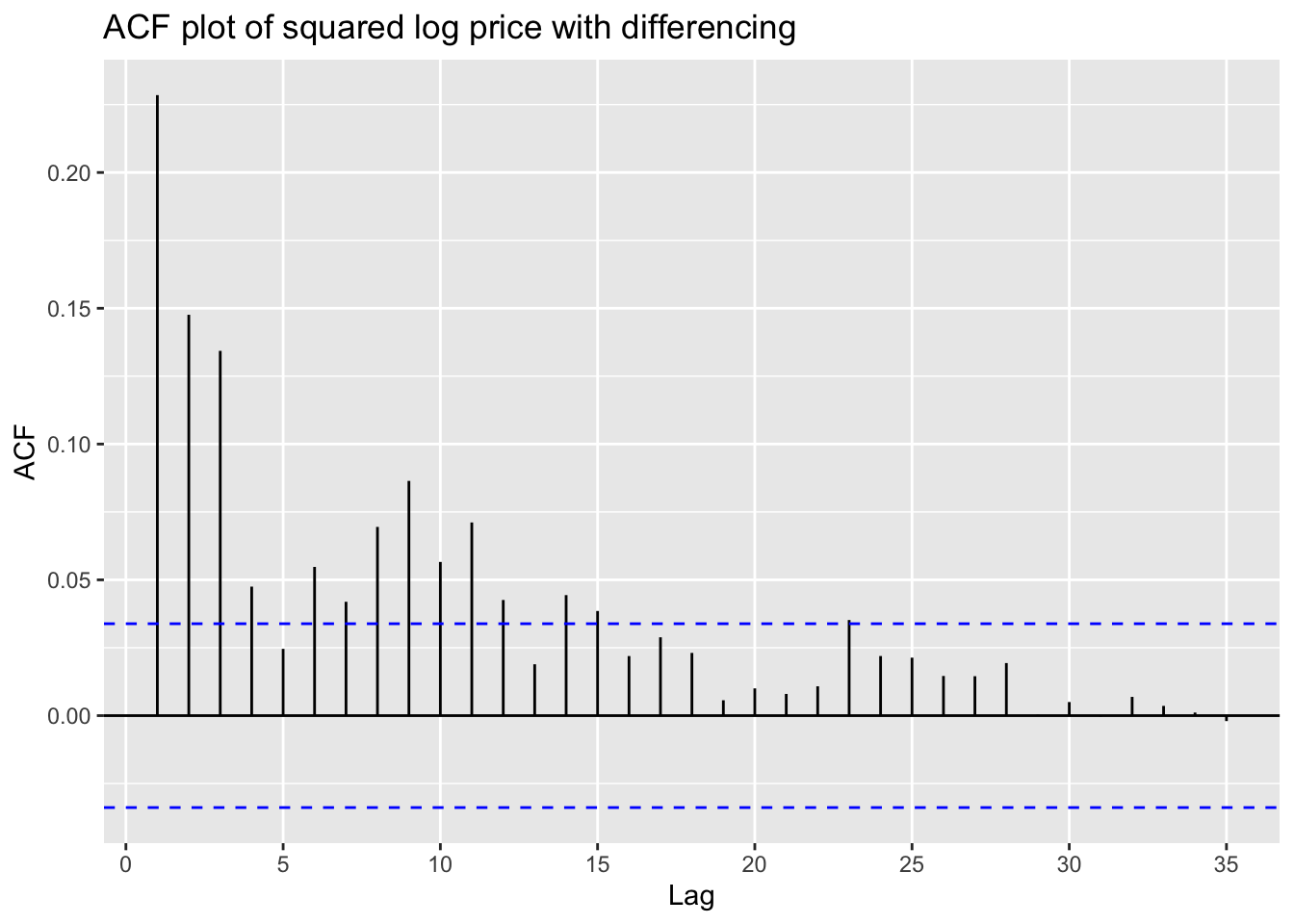

ggAcf(returns^2)+ggtitle("ACF plot of squared log price with differencing")

These plots above shows that an ARIMA model is needed for fitting this stock price data.

3 ARIMA model fitting

Next, I will try to fit a series of ARIMA models with different parameters and determine the best model based on AIC, BIC and AICc values.

Code

log.WMT=log(WMT.close)

i=1

temp= data.frame()

ls=matrix(rep(NA,6*18),nrow=18)

for (p in 0:2)

{

for(q in 0:2)

{

for(d in 0:1)

{

if(p+d+q<=8)

{

model<- Arima(log.WMT,order=c(p,d,q),include.drift=TRUE)

ls[i,]= c(p,d,q,model$aic,model$bic,model$aicc)

i=i+1

}

}

}

}

temp= as.data.frame(ls)

names(temp)= c("p","d","q","AIC","BIC","AICc")

#temp

knitr::kable(temp)| p | d | q | AIC | BIC | AICc |

|---|---|---|---|---|---|

| 0 | 0 | 0 | -4787.751 | -4769.397 | -4787.744 |

| 0 | 1 | 0 | -20009.436 | -19997.201 | -20009.433 |

| 0 | 0 | 1 | -8966.713 | -8942.241 | -8966.701 |

| 0 | 1 | 1 | -20017.978 | -19999.625 | -20017.971 |

| 0 | 0 | 2 | -11889.597 | -11859.008 | -11889.579 |

| 0 | 1 | 2 | -20016.002 | -19991.532 | -20015.990 |

| 1 | 0 | 0 | -20016.607 | -19992.135 | -20016.595 |

| 1 | 1 | 0 | -20018.012 | -19999.659 | -20018.005 |

| 1 | 0 | 1 | -20024.177 | -19993.587 | -20024.159 |

| 1 | 1 | 1 | -20016.000 | -19991.530 | -20015.988 |

| 1 | 0 | 2 | -20022.267 | -19985.560 | -20022.242 |

| 1 | 1 | 2 | -20014.008 | -19983.420 | -20013.990 |

| 2 | 0 | 0 | -20024.252 | -19993.663 | -20024.234 |

| 2 | 1 | 0 | -20016.013 | -19991.543 | -20016.001 |

| 2 | 0 | 1 | -20022.280 | -19985.572 | -20022.254 |

| 2 | 1 | 1 | -20014.013 | -19983.425 | -20013.995 |

| 2 | 0 | 2 | -20020.204 | -19977.378 | -20020.170 |

| 2 | 1 | 2 | -20014.629 | -19977.923 | -20014.604 |

Model with minimum AIC:

Code

temp[which.min(temp$AIC),] p d q AIC BIC AICc

13 2 0 0 -20024.25 -19993.66 -20024.23Model with minimum BIC:

Code

temp[which.min(temp$BIC),] p d q AIC BIC AICc

8 1 1 0 -20018.01 -19999.66 -20018.01Model with minimum AICc:

Code

temp[which.min(temp$AICc),] p d q AIC BIC AICc

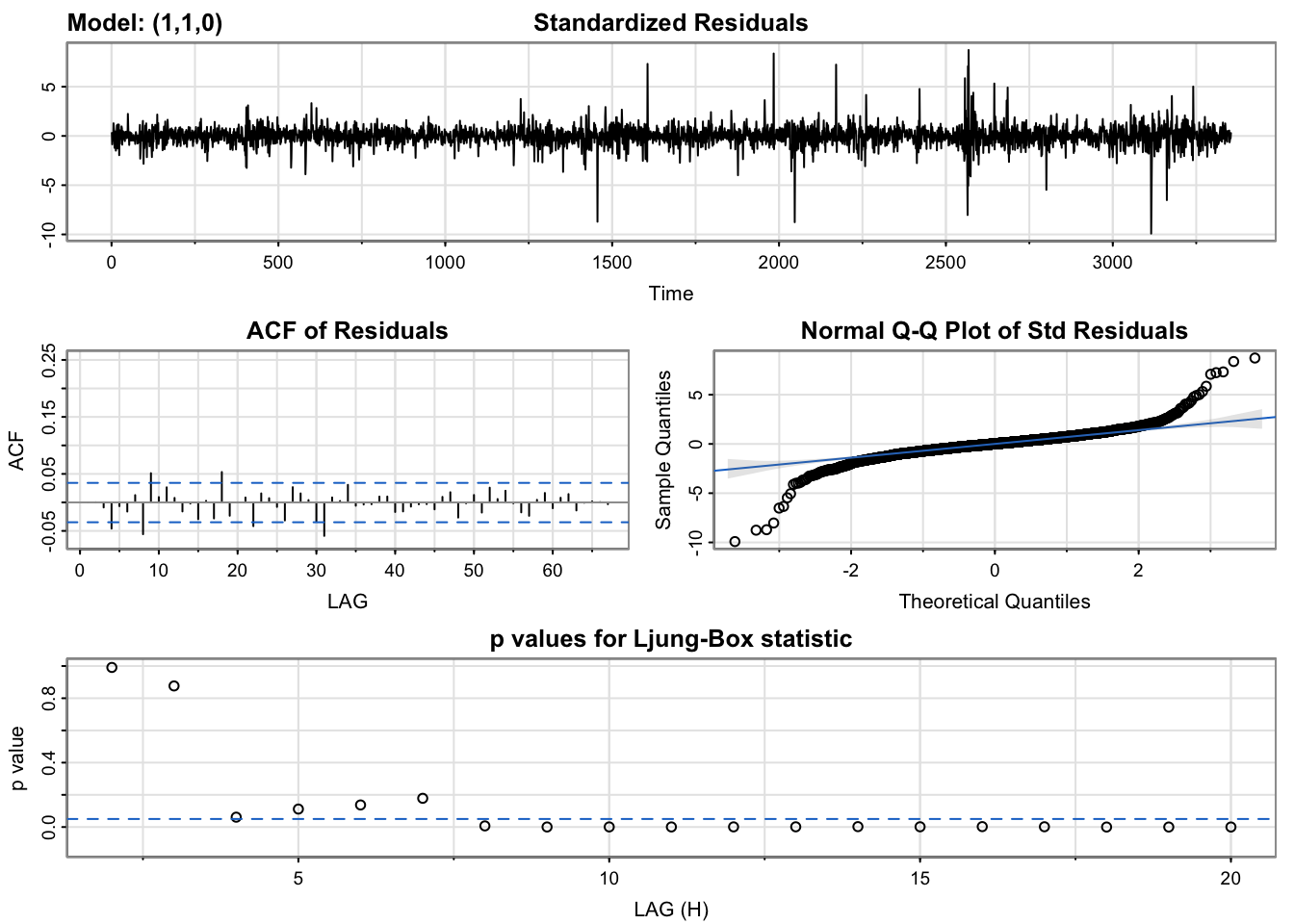

13 2 0 0 -20024.25 -19993.66 -20024.23The results shows that ARIMA(2,0,0) has minimum AIC and AICc values, while ARIMA(1,1,0) has the minimum BIC value. Now compare the two models using model diagnostics.

- ARIMA(1,1,0) model:

Code

sarima(log.WMT,1,1,0)initial value -4.403305

iter 2 value -4.404882

iter 2 value -4.404882

iter 2 value -4.404882

final value -4.404882

converged

initial value -4.404923

iter 1 value -4.404923

final value -4.404923

converged

$fit

Call:

arima(x = xdata, order = c(p, d, q), seasonal = list(order = c(P, D, Q), period = S),

xreg = constant, transform.pars = trans, fixed = fixed, optim.control = list(trace = trc,

REPORT = 1, reltol = tol))

Coefficients:

ar1 constant

-0.0561 4e-04

s.e. 0.0172 2e-04

sigma^2 estimated as 0.0001493: log likelihood = 10012.01, aic = -20018.01

$degrees_of_freedom

[1] 3351

$ttable

Estimate SE t.value p.value

ar1 -0.0561 0.0172 -3.2545 0.0011

constant 0.0004 0.0002 1.9768 0.0481

$AIC

[1] -5.97018

$AICc

[1] -5.970179

$BIC

[1] -5.964706- ARIMA(2,0,0) model:

Code

sarima(log.WMT,2,0,0)initial value -0.871503

iter 2 value -0.872504

iter 3 value -4.313351

iter 4 value -4.313868

iter 5 value -4.376908

iter 6 value -4.401093

iter 7 value -4.404339

iter 8 value -4.404343

iter 8 value -4.404343

final value -4.404343

converged

initial value -4.403196

iter 1 value -4.403196

final value -4.403196

converged

$fit

Call:

arima(x = xdata, order = c(p, d, q), seasonal = list(order = c(P, D, Q), period = S),

xreg = xmean, include.mean = FALSE, transform.pars = trans, fixed = fixed,

optim.control = list(trace = trc, REPORT = 1, reltol = tol))

Coefficients:

ar1 ar2 xmean

0.9449 0.0548 4.3072

s.e. 0.0172 0.0172 0.3959

sigma^2 estimated as 0.0001494: log likelihood = 10009.2, aic = -20010.4

$degrees_of_freedom

[1] 3351

$ttable

Estimate SE t.value p.value

ar1 0.9449 0.0172 54.7973 0.0000

ar2 0.0548 0.0172 3.1790 0.0015

xmean 4.3072 0.3959 10.8783 0.0000

$AIC

[1] -5.96613

$AICc

[1] -5.966128

$BIC

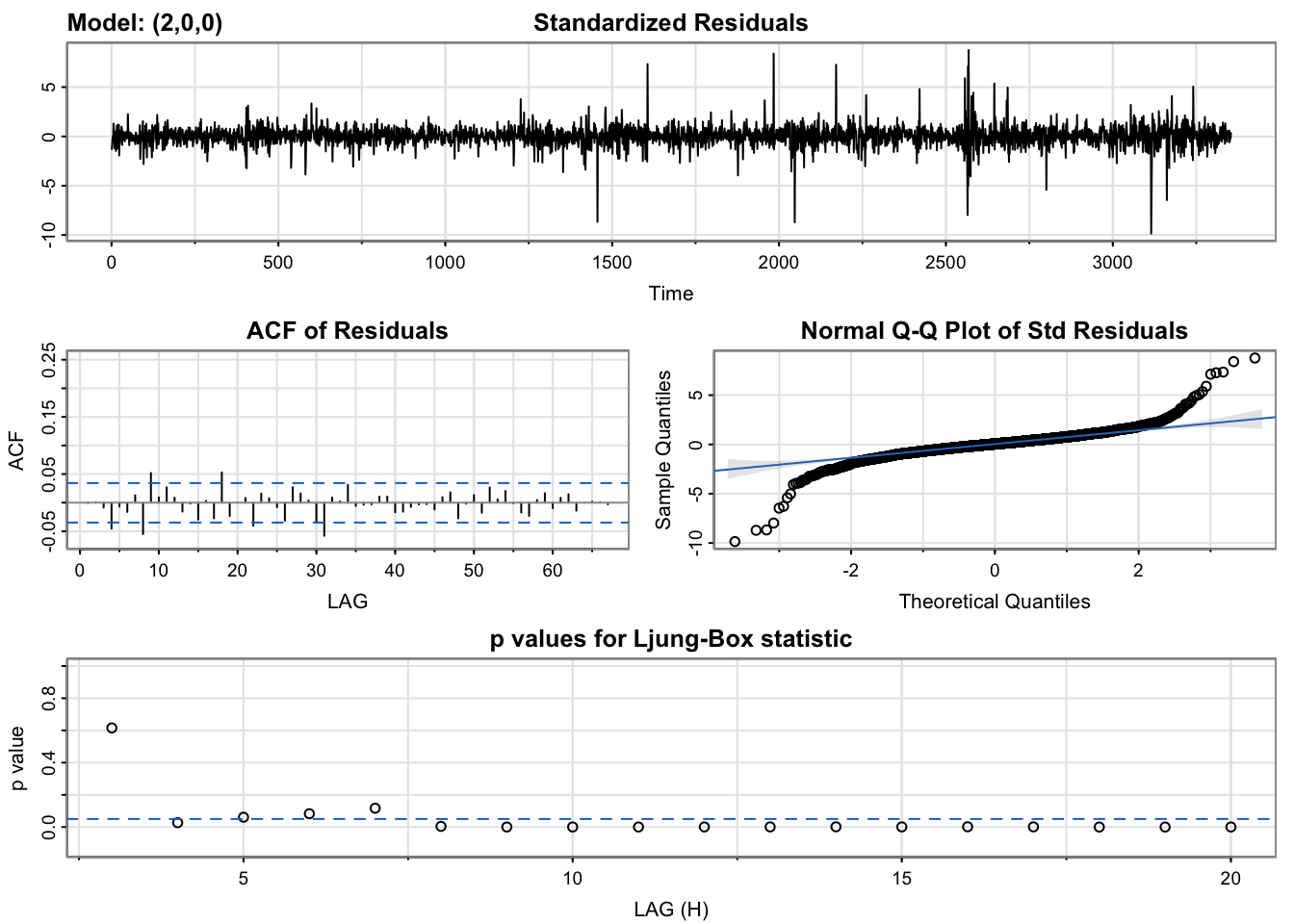

[1] -5.958834According to model diagnostics of these two models, we can see that both models perform relatively good. The residuals of both models have good normality and coefficients in these two models are all significant. However, from the Ljung-Box test, ARIMA(1,1,0) has more values greater than 0.05, which means the residuals of this model are more likely to be independent. Thus, I will choose ARIMA(1,1,0) as the optimal model.

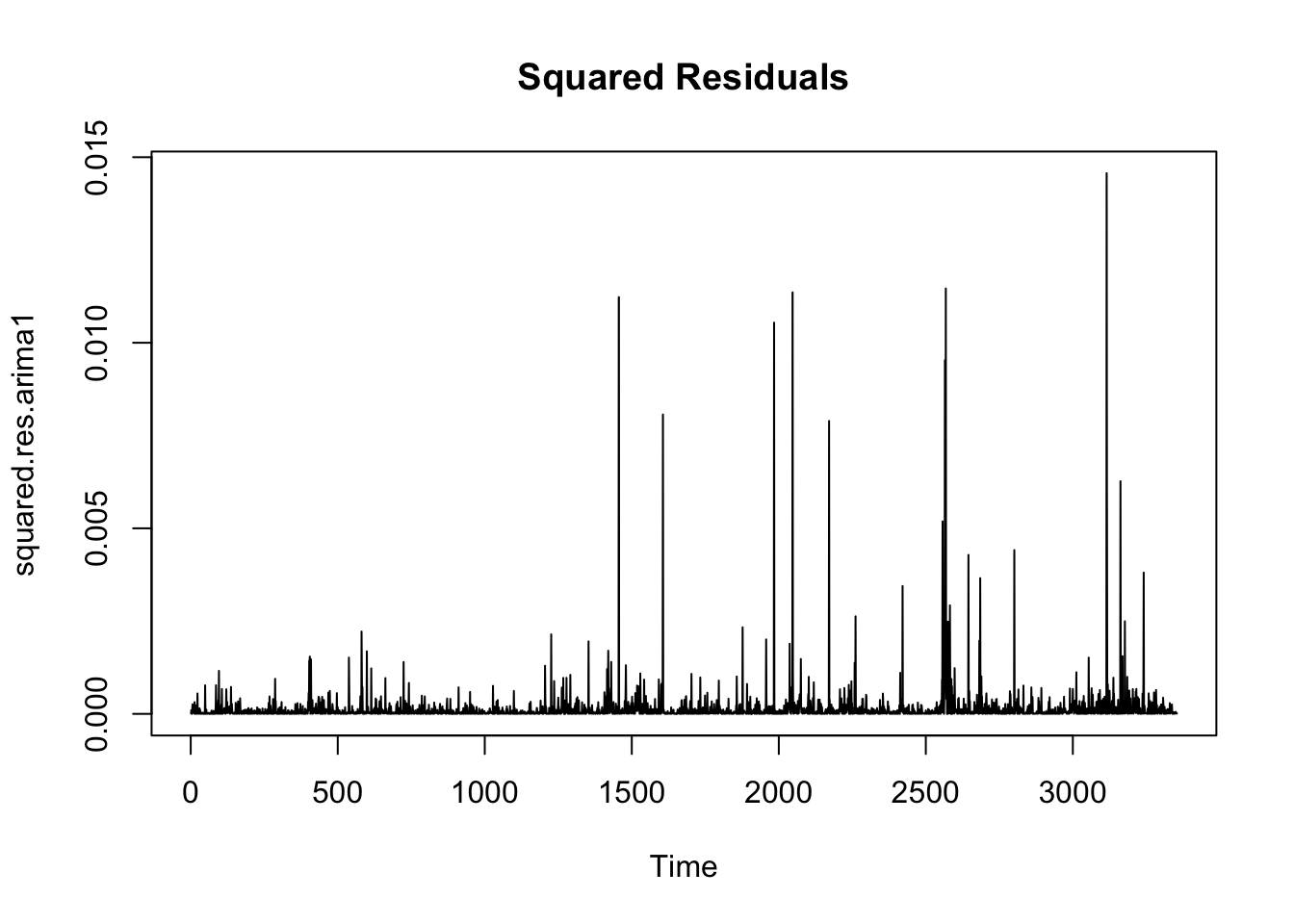

The squared residuals of this model is as follows:

Code

arima1=arima(log.WMT,order=c(1,1,0))

res.arima1=arima1$res

squared.res.arima1=res.arima1^2

plot(squared.res.arima1,main='Squared Residuals')

Obviously, an ARCH model is needed for fitting the residuals of ARIMA model.

4 ARCH model fitting

In following part, I will sequentially fit ARCH models with different parameters and determine the best one based on AIC value.

Code

ARCH <- list()

i=1

for (p in 1:10) {

ARCH[[i]] <- garch(res.arima1,order=c(0,p),trace=F)

i=i+1

}

## get AIC values for model evaluation

ARCH_AIC <- sapply(ARCH, AIC) Minimum AIC value:

[1] -20477.34The parameter of model with minimum AIC value:

[1] 8This means ARCH(8) fits the residual best. Have a look at the summary of this model.

Code

arch8=garch(res.arima1,order=c(0,8),trace=F)

summary(arch8)

Call:

garch(x = res.arima1, order = c(0, 8), trace = F)

Model:

GARCH(0,8)

Residuals:

Min 1Q Median 3Q Max

-10.21902 -0.49084 0.05551 0.56775 9.64066

Coefficient(s):

Estimate Std. Error t value Pr(>|t|)

a0 7.317e-05 2.101e-06 34.819 < 2e-16 ***

a1 1.187e-01 1.289e-02 9.212 < 2e-16 ***

a2 4.500e-02 1.274e-02 3.532 0.000413 ***

a3 6.045e-02 1.156e-02 5.230 1.70e-07 ***

a4 6.918e-02 1.453e-02 4.761 1.93e-06 ***

a5 1.663e-13 9.013e-03 0.000 1.000000

a6 1.103e-02 1.050e-02 1.050 0.293590

a7 1.060e-01 7.161e-03 14.802 < 2e-16 ***

a8 1.018e-01 1.172e-02 8.687 < 2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Diagnostic Tests:

Jarque Bera Test

data: Residuals

X-squared = 25923, df = 2, p-value < 2.2e-16

Box-Ljung test

data: Squared.Residuals

X-squared = 0.0079708, df = 1, p-value = 0.9289The p-value of Box-Ljung test is much greater than 0.05, suggesting that this model has adequately represents the residual. Also, most coefficients within this model are significant except a5 and a6.

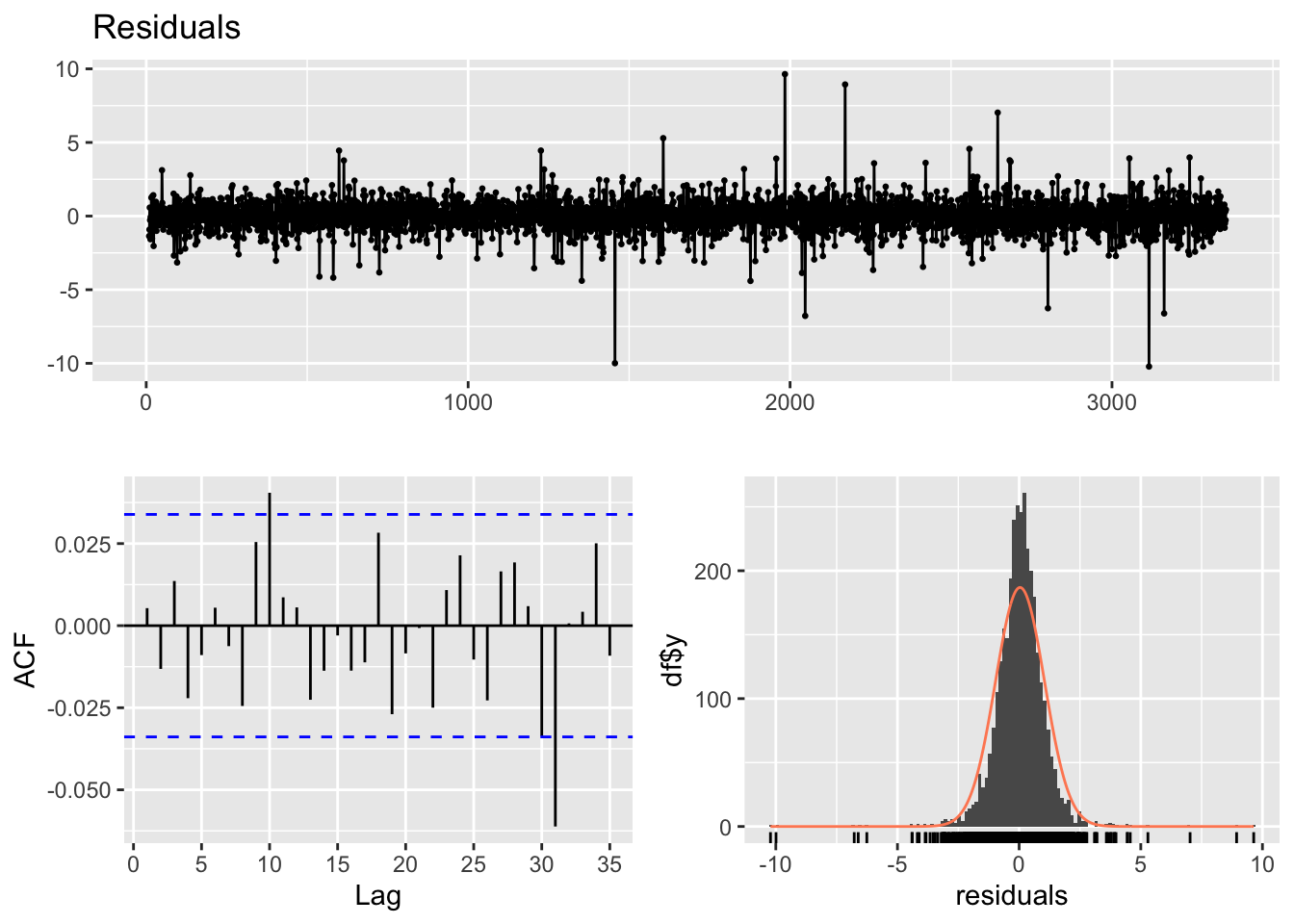

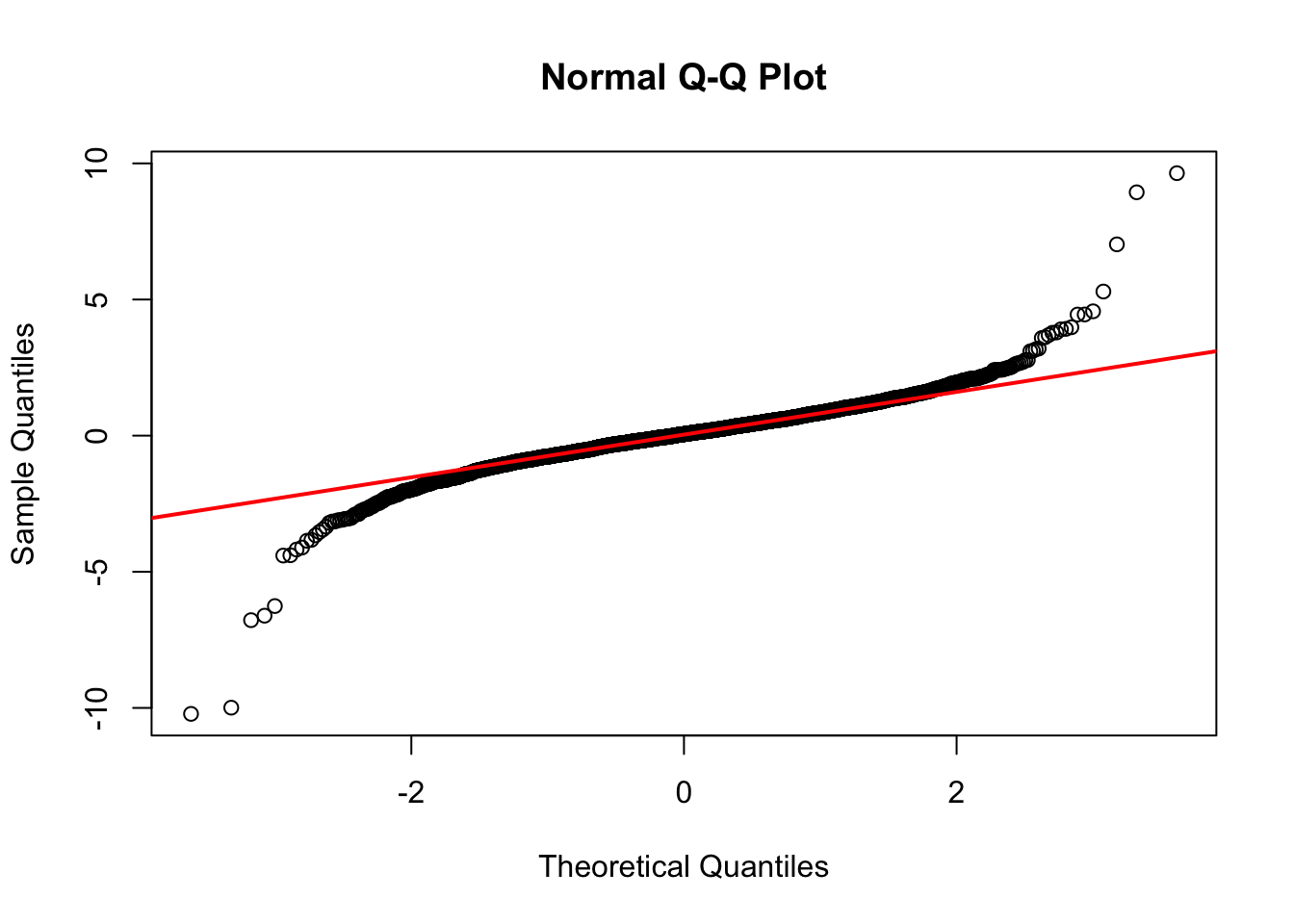

5 Model diagnostics and conclusions

Finally, have a look at the model diagnostics of the whole ARIMA(1,1,0)+ARCH(8) for this stock price data to check the model performance.

Code

checkresiduals(arch8)

Code

qqnorm(arch8$residuals, pch=1)

qqline(arch8$residuals, col="red", lwd=2)

Code

Box.test(arch8$residuals, type="Ljung-Box")

Box-Ljung test

data: arch8$residuals

X-squared = 0.095367, df = 1, p-value = 0.7575These plots and test all show strong signals that the model performs quite well. From the residual plot, we can see relatively constant mean and variance. Next, the ACF plot shows good stationarity within the residuals. Besides, the distribution of the residuals and QQ-plot indicate that the residuals almost follow a normal distribution. Finally, the p-value of Box-Ljung test is much greater than 0.05, meaning that the residuals are independent.

6 Model equations

The equations of the ARIMA(1,1,0)+ARCH(8) model can be written as follows:

\[ (1-\phi_1B)(1-B)x_t=y_t+\delta \]

\[ y_t=\sigma_t \epsilon_t \]

\[ \sigma^2=a_0+a_1y_{t-1}^2+a_2y_{t-2}^2+a_3y_{t-3}^2+\cdots+a_8y_{t-8}^2 \]

In these equations, \(\phi_1\) eqauls to -0.0561. The coefficients of the third equations are listed below:

[[1]]

Call:

garch(x = res.arima1, order = c(0, p), trace = F)

Coefficient(s):

a0 a1 a2 a3 a4 a5 a6

7.317e-05 1.187e-01 4.500e-02 6.045e-02 6.918e-02 1.663e-13 1.103e-02

a7 a8

1.060e-01 1.018e-01 7 Stock price and sales

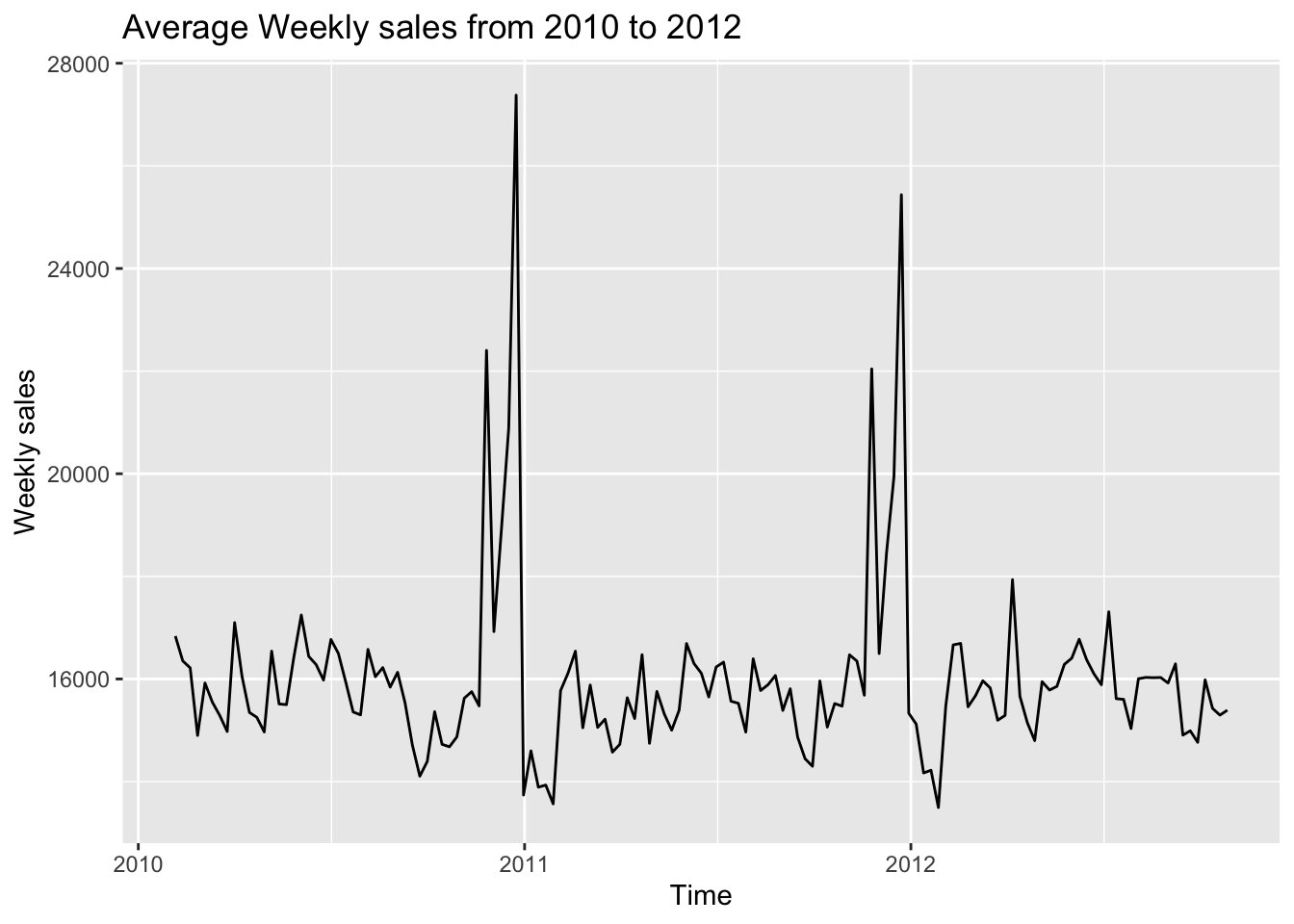

In this section, I will compare the visualizations of stock price and weekly sales, in order to figure out if these two time series have something in common. The observation time is from 2010-02 to 2012-10.

[1] "WMT"Code

chartSeries(WMT, theme = chartTheme("white"),

bar.type = "hlc",

up.col = "green",

dn.col = "red")

Code

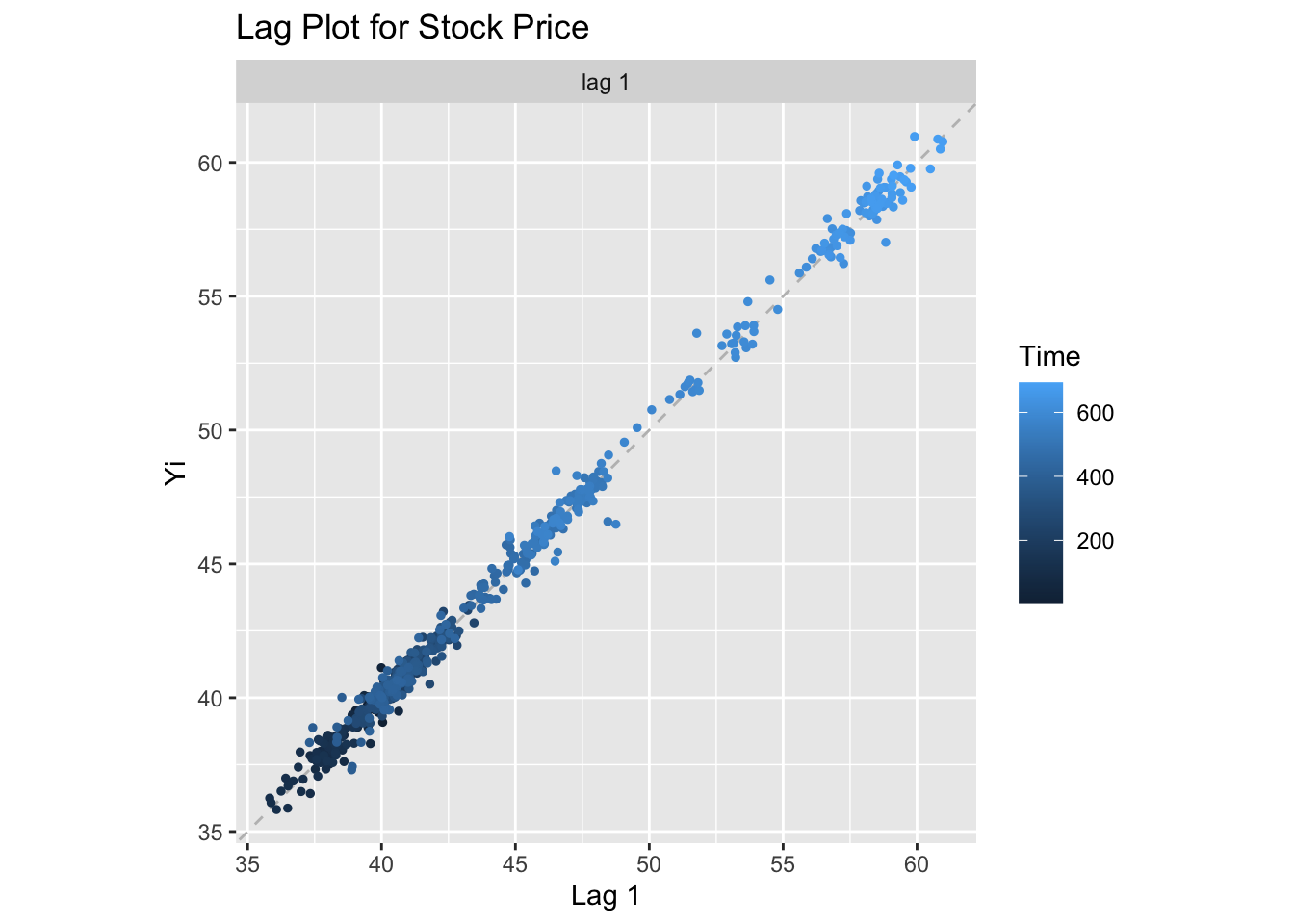

gglagplot(WMT.close, do.lines=FALSE, lags=1)+xlab("Lag 1")+ylab("Yi")+ggtitle("Lag Plot for Stock Price")

The candlestick plot and lag plot indicate that the stock price of Walmart from 2010 to 2012 has a obvious upward trend. However, the “decompose” function failed to decompose this time series into different components, suggesting that seasonality does not exist in this time series.

Code

walmart=read.csv("./data/Walmart_sales_data.csv")

bytime=group_by(walmart,Date)

sales=summarise(bytime,avg = mean(Weekly_Sales))

sales$Date=as.Date(sales$Date)

ggplot(sales,aes(x=Date,y=avg))+

geom_line()+

labs(

x = "Time",

y = "Weekly sales"

)+

ggtitle("Average Weekly sales from 2010 to 2012")

This plot above, which we are already very familiar, displays the average weekly sales of all the stores from 2010 to 2012. This time series of weekly sales has significant seasonal components rather than trend, which is absolutely opposite to the stock price data. Therefore, we can not observe any relationship between the stock price of Walmart and the weekly sales of given stores.